Borrowing money is easier today than ever before. With credit cards, personal loans, buy now, pay later services, and financing options available almost everywhere, it’s tempting to spend now and pay later. But before taking on debt, it’s important to ask yourself: explain why debt and credit are a bad idea. How could they negatively affect your life?

The answer isn’t that debt or credit are always bad. In fact, they can be useful financial tools when managed responsibly. However, relying too heavily on borrowed money or using credit without a clear repayment plan can lead to financial stress, damaged credit, and fewer opportunities in the future. This article explores the risks of debt and credit, how they can affect different areas of your life, and practical ways to avoid common financial mistakes.

Understanding Debt and Credit

Before discussing the drawbacks, it’s helpful to understand the difference between debt and credit.

- Credit is the ability to borrow money or access goods and services with the promise of paying later.

- Debt is the amount of money you owe after using credit.

Common forms of credit include:

- Credit cards

- Personal loans

- Car loans

- Student loans

- Mortgages

- Buy Now, Pay Later (BNPL) services

- Lines of credit

Credit itself isn’t harmful. Problems arise when debt becomes difficult to manage or repay.

Explain Why Debt and Credit Are a Bad Idea

When people ask, “Explain why debt and credit are a bad idea. How could they negatively affect your life?”, they’re usually referring to the risks of borrowing more than you can comfortably repay.

Here are some of the most significant disadvantages.

1. Debt Can Become Expensive

One of the biggest problems with debt is interest.

When you borrow money, you usually pay back:

- The original amount borrowed

- Interest charges

- Possible fees

Over time, interest can make purchases much more expensive than their original price.

For example, carrying a balance on a high-interest credit card can significantly increase the total amount you repay.

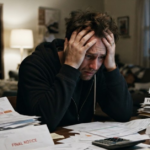

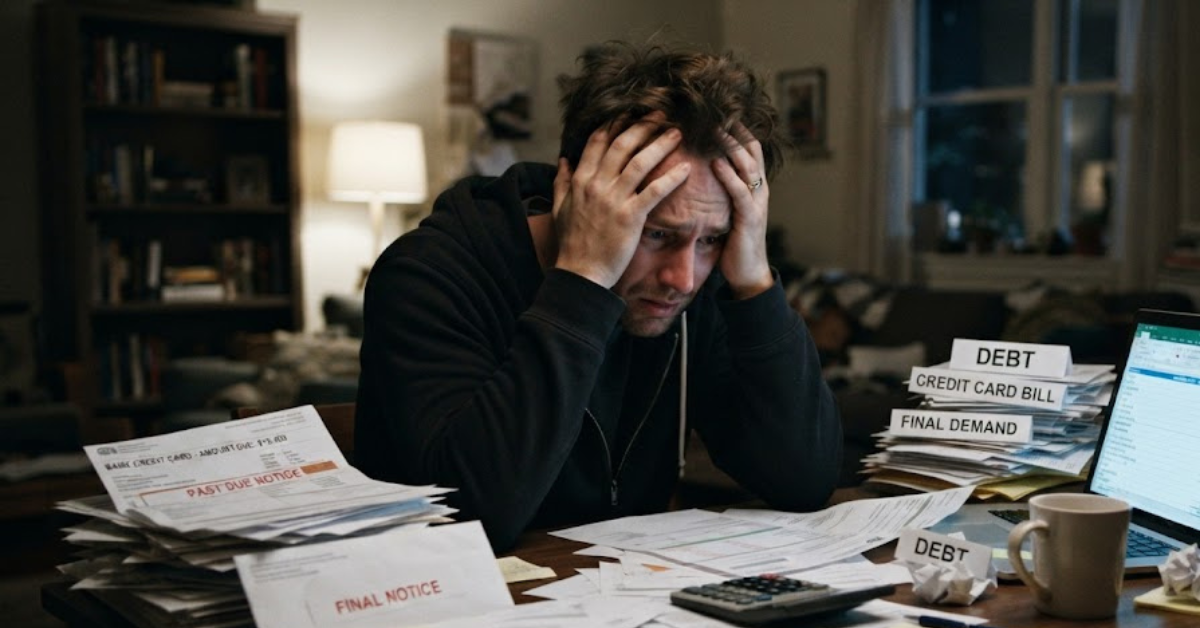

2. Financial Stress and Anxiety

Money problems are one of the leading causes of stress.

Large debts can create constant worry about:

- Monthly repayments

- Unexpected bills

- Collection notices

- Meeting everyday expenses

Financial stress can affect sleep, relationships, productivity, and overall well-being.

3. Reduced Financial Freedom

Every loan payment reduces the money available for other priorities.

Instead of saving or investing, you may spend a large portion of your income repaying debt.

This can make it harder to:

- Build an emergency fund

- Save for retirement

- Travel

- Buy a home

- Start a business

Debt limits financial flexibility.

4. Damage to Your Credit Score

Although credit can help build a positive credit history, mismanaging it can have the opposite effect.

Missing payments or defaulting on loans may lower your credit score.

A poor credit history can make it more difficult to:

- Qualify for future loans

- Rent a property

- Obtain lower interest rates

- Access certain financial products

5. Paying for Yesterday’s Purchases

One hidden danger of credit is paying for items long after you’ve stopped using them.

For example, if you finance:

- Clothes

- Electronics

- Vacations

- Entertainment

You could still be making payments months—or even years—later.

This creates a cycle where future income pays for past spending.

6. Increased Risk of Overspending

Credit often makes spending feel easier because you don’t immediately part with your own money.

Psychologically, people tend to spend more when using credit compared to paying with cash or debit cards.

Without careful budgeting, it’s easy to accumulate balances that become difficult to repay.

7. Debt Can Delay Life Goals

High debt levels may postpone important milestones, such as:

- Buying your first home

- Starting a family

- Changing careers

- Launching a business

- Retiring comfortably

Monthly repayments can reduce your ability to pursue long-term goals.

8. Potential Legal Consequences

If debts remain unpaid, lenders may take action depending on local laws and the type of debt.

Possible consequences include:

- Collection activity

- Additional fees

- Legal proceedings

- Wage garnishment (where permitted by law)

- Repossession of secured assets, such as vehicles

Ignoring debt rarely makes it disappear.

Emotional Effects of Debt

Debt affects more than your finances.

Many people experience:

- Anxiety

- Depression

- Embarrassment

- Relationship conflict

- Reduced confidence

- Constant worry

Financial pressure can have a significant impact on mental health if left unmanaged.

How Credit Can Be Misused

Credit becomes problematic when it’s used to support a lifestyle that isn’t affordable.

Examples include:

- Buying luxury items you can’t comfortably afford

- Making only minimum credit card payments

- Frequently using payday loans

- Borrowing to pay off existing debt without a repayment strategy

- Relying on credit for everyday expenses because of poor budgeting

Responsible borrowing means understanding both the costs and your ability to repay.

When Debt Can Be Helpful

It’s important to remember that debt isn’t always negative.

Used wisely, it can help finance investments that provide long-term value.

Examples include:

- Education that improves career opportunities

- A reasonably priced home mortgage

- A business loan with a solid business plan

- A car loan needed for reliable transportation to work

The key difference is borrowing for needs or investments rather than unnecessary spending.

Tips to Avoid Debt Problems

Good financial habits can reduce the risk of excessive debt.

Consider these strategies:

- Create a monthly budget.

- Spend less than you earn.

- Build an emergency savings fund.

- Pay credit card balances in full whenever possible.

- Avoid impulse purchases.

- Compare loan interest rates before borrowing.

- Borrow only what you can realistically repay.

- Review your finances regularly.

Small financial decisions today can have a big impact in the future.

Signs Your Debt May Be Becoming a Problem

Watch for these warning signs:

- You’re making only minimum payments.

- You borrow to pay other debts.

- You regularly miss payment deadlines.

- Most of your income goes toward repayments.

- You avoid checking bank statements or bills.

- You’re relying on credit for everyday living expenses.

Recognizing these signs early allows you to seek help before the situation worsens.

Common Myths About Debt and Credit

Myth: All Debt Is Bad

Not necessarily. Responsible borrowing for worthwhile investments can be beneficial.

Myth: Credit Cards Are Free Money

Every purchase must eventually be repaid, often with interest if the balance isn’t paid in full.

Myth: Minimum Payments Solve the Problem

Paying only the minimum often increases the total interest paid and extends repayment for years.

Myth: Good Income Prevents Debt Problems

Even high earners can experience financial difficulty if they consistently spend more than they earn.

FAQs

Explain why debt and credit are a bad idea. How could they negatively affect your life?

Debt and credit can negatively affect your life by increasing financial stress, creating expensive interest costs, reducing financial freedom, damaging your credit history if repayments are missed, and delaying important life goals. While credit can be useful, it becomes harmful when borrowing exceeds your ability to repay.

Is all debt bad?

No. Some forms of debt, such as a reasonable mortgage, education loan, or business loan, can provide long-term benefits when managed responsibly.

How does debt affect mental health?

Excessive debt can contribute to stress, anxiety, sleep problems, and relationship difficulties due to ongoing financial pressure.

Can credit help build a good credit score?

Yes. Using credit responsibly and making payments on time can help build a positive credit history.

Why is credit card debt considered risky?

Credit cards often have relatively high interest rates. Carrying balances over time can make even small purchases much more expensive.

How can I avoid getting into debt?

Create a budget, spend within your means, save for emergencies, avoid unnecessary borrowing, and pay bills on time.

What’s the difference between good debt and bad debt?

Good debt is typically used to finance assets or opportunities that may increase in value or improve earning potential, while bad debt is often associated with unnecessary spending on depreciating items or purchases that don’t provide long-term financial benefits.

Conclusion

When asked to explain why debt and credit are a bad idea. How could they negatively affect your life?, the most balanced answer is that debt and credit are financial tools that require careful management. Used irresponsibly, they can lead to costly interest, financial stress, damaged credit, reduced savings, and delayed life goals. On the other hand, responsible borrowing for meaningful investments—such as education or home ownership—can support long-term financial success.

The key is to borrow only when necessary, understand the true cost of credit, and develop healthy financial habits. By living within your means, budgeting wisely, and making informed borrowing decisions, you can avoid many of the challenges associated with debt while building a stronger financial future.